Unused TFSA and RRSP contribution room: how backdated years carry forward

Here is the question I hear most from Canadians who open their first brokerage account: "I never used my TFSA or RRSP. Can I go back and contribute for all those past years?" The short version is yes, you almost certainly have room saved up from years you skipped. But TFSAs and RRSPs build that backdated room in completely different ways, and mixing them up is how people end up with a penalty letter from the CRA.

So let's walk through it properly. I'll show you the contribution limit for every year, how the unused room stacks up into one running total, the rules that decide how much of it is actually yours, and exactly where to find your own number. There are charts, year-by-year tables, and links to the CRA pages so you can verify everything yourself.

What's in this guide

| Section | What it covers |

|---|---|

| The short answer | Both carry forward, but they are not the same animal |

| TFSA room by year | Every annual limit since 2009 and the $109,000 running total |

| RRSP room by year | Why your backdated RRSP room depends on income |

| TFSA vs RRSP carry-forward | The differences that actually matter |

| Find your real number | CRA My Account, your NOA, and why they can be wrong |

| Mistakes that cost money | Over-contributions, recontribution timing, and more |

| What to hold where | Room is step one; the stock you put in it is step two |

| FAQ | Quick answers to the common questions |

| Sources | The official CRA references |

The short answer: yes, but they don't work the same way

Both the TFSA and the RRSP let you carry unused contribution room forward, so years you skipped are not lost. That's the good news, and it's true for almost everyone.

The catch is in how each one builds room in the first place. Your TFSA room is handed to you on a schedule. Every year you're 18 or older and a resident of Canada, you get that year's TFSA dollar limit, full stop. Your income has nothing to do with it. The RRSP is the opposite. You only earn RRSP room when you have "earned income," and the amount is 18% of the prior year's earned income up to an annual cap. No income in a given year means basically no new RRSP room for the next one.

So "backdated room" means two different things. For the TFSA it's just the sum of the limits for every year you were eligible. For the RRSP it's the leftover deduction limit that built up in the years you were working but didn't contribute. Keep that distinction in your head and the rest of this is easy.

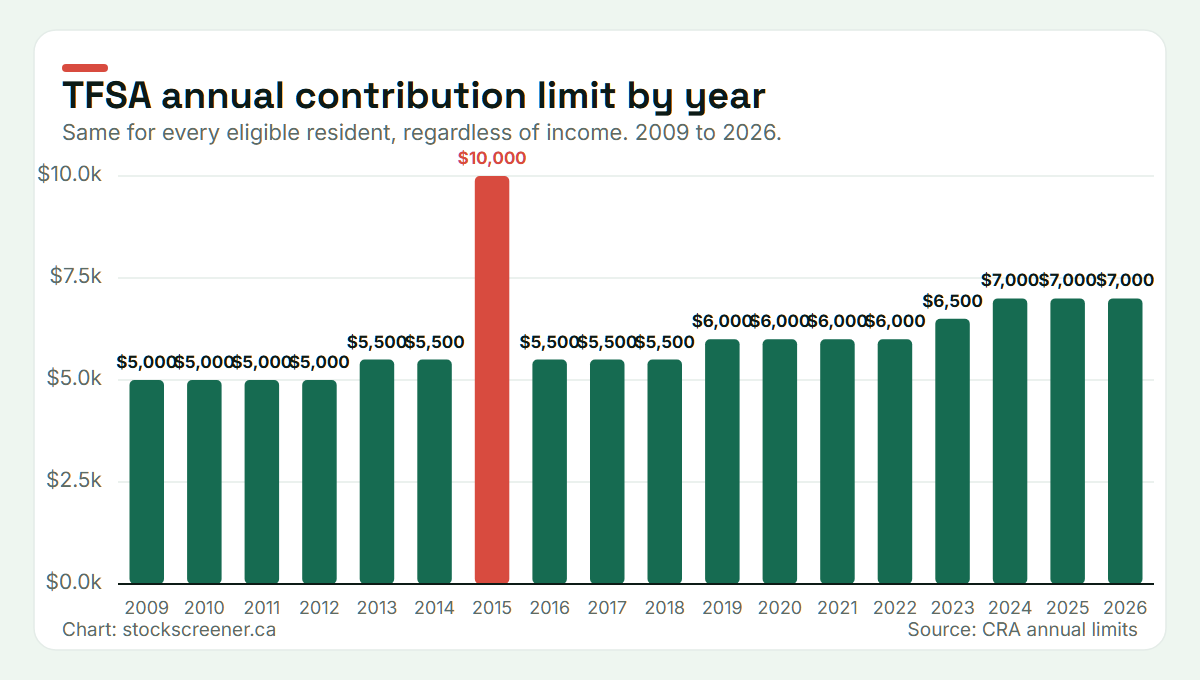

TFSA room by year: the backdated years just stack up

The TFSA launched in 2009. Since then the annual limit has moved around a bit, mostly tracking inflation, with one big one-time bump to $10,000 in 2015 that lasted a single year. Here's every year.

| Years | Annual TFSA limit |

|---|---|

| 2009, 2010, 2011, 2012 | $5,000 |

| 2013, 2014 | $5,500 |

| 2015 | $10,000 |

| 2016, 2017, 2018 | $5,500 |

| 2019, 2020, 2021, 2022 | $6,000 |

| 2023 | $6,500 |

| 2024, 2025, 2026 | $7,000 |

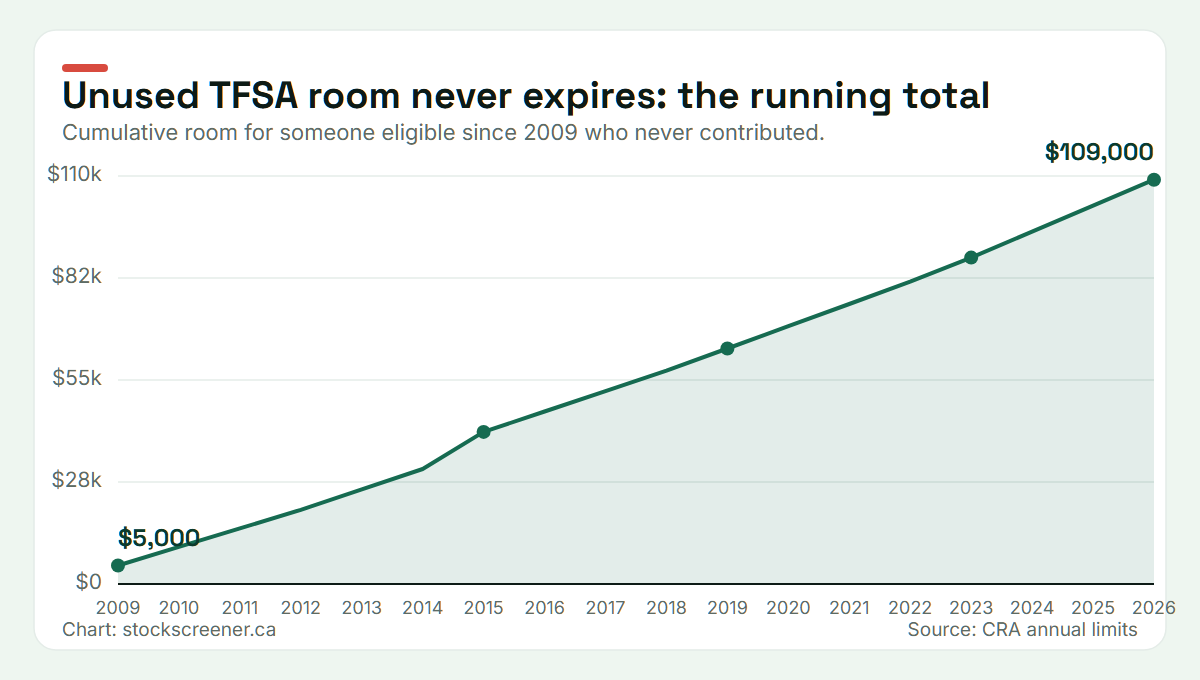

Now the part people actually care about. Because unused room never expires, those numbers add together into one running total. If you were at least 18 and a Canadian resident in 2009, and you've never put a dollar into a TFSA, your cumulative room in 2026 is $109,000. That is not a typo. It really is more than a hundred thousand dollars of tax-free contribution room sitting there waiting.

A few rules decide how much of that $109,000 is actually yours:

- You start accumulating at 18. If you turned 18 after 2009, your room is the sum of the limits from your eighteenth year onward, not the full $109,000. You can't backdate room to years before you were 18.

- Residency counts. You build TFSA room only for years you were a Canadian resident. If you lived abroad for a stretch, those years generally don't count.

- Withdrawals come back, but not right away. When you take money out of a TFSA, that amount gets added back to your room, but only on January 1 of the following year. Pulling out and putting back in the same calendar year is the single most common way people over-contribute by accident.

Here's a quick worked example. Say you turned 18 in 2016. You don't get the 2009 through 2015 limits, because those years happened before you were eligible. Your room is the sum from 2016 on: $5,500 each for 2016, 2017 and 2018, then $6,000 each for 2019 through 2022, $6,500 in 2023, and $7,000 each for 2024, 2025 and 2026. Add it up and you've got $68,000 of room in 2026, assuming you never contributed and stayed a resident. Different starting year, different number, same method.

Let me make the withdrawal rule concrete, because it trips people up more than anything else here. Suppose you'd maxed your TFSA, then pulled out $20,000 in June 2026 for a house deal that fell through. You can't just put that $20,000 back in 2026. It returns to your room on January 1, 2027. Re-deposit it in 2026 and the CRA treats it as a $20,000 over-contribution, taxed at 1% per month until you fix it. Wait for the new year and the exact same deposit is completely fine. The money didn't change. The timing did.

One thing the TFSA does not care about is what you earn. A student with a part-time job and a high earner accumulate the exact same TFSA room. That's worth repeating because it's the opposite of how the RRSP works.

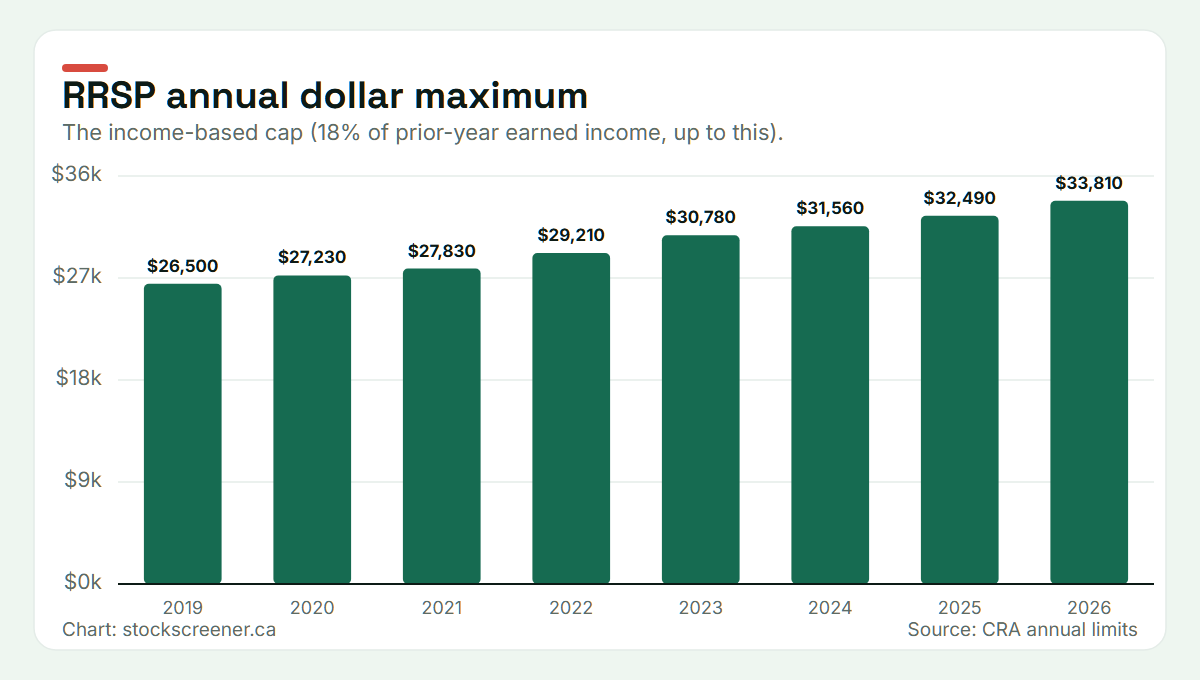

RRSP room by year: backdated, but only if you earned income

RRSP room carries forward too, and it carries forward indefinitely until the year you turn 71 (the year your RRSP has to be converted to a RRIF or annuity). So if you've been working for a decade and barely touched your RRSP, you've likely got a big stack of unused room.

But here's where it splits from the TFSA. Your RRSP room for a year is 18% of the "earned income" you reported the year before, capped at an annual dollar maximum, then reduced by any pension adjustment if you're in a workplace pension. Earned income mostly means employment and self-employment income. It does not include things like most investment income. The annual dollar caps have climbed steadily.

| Year | RRSP dollar maximum |

|---|---|

| 2019 | $26,500 |

| 2020 | $27,230 |

| 2021 | $27,830 |

| 2022 | $29,210 |

| 2023 | $30,780 |

| 2024 | $31,560 |

| 2025 | $32,490 |

| 2026 | $33,810 |

Read the dollar cap as a ceiling, not your number. You only hit it if 18% of your prior-year earned income reaches that high. For 2026, you'd need roughly $187,800 of earned income in 2025 to max out the $33,810 cap. Most people's actual room is 18% of whatever they earned, plus everything they didn't use in past years.

There's also a small cushion worth knowing about: the CRA generally allows a lifetime $2,000 over-contribution buffer on RRSPs before penalties kick in. It's not contribution room you can deduct, and I wouldn't lean on it, but it's why a tiny accidental over-contribution usually isn't a disaster. The TFSA has no such buffer. Go over on a TFSA and the penalty starts immediately.

A worked example helps on the RRSP side too. Say you earned $75,000 in 2025 and you're not in a workplace pension. Your new RRSP room for 2026 is 18% of $75,000, which is $13,500, well under the $33,810 cap. Now say you also have $40,000 of unused room stacked up from earlier working years you didn't contribute in. Your total room for 2026 is $53,500. That's the backdated room doing its job. And from a tax angle you don't have to deduct it all at once. You can contribute now and carry the deduction forward to a year you're in a higher bracket, which is sometimes the smarter play.

Two timing details are worth knowing. Contributions made in the first 60 days of a year can be deducted on either that year's return or the previous one, which is why you see the RRSP "deadline" headlines every February. And unlike a TFSA, an RRSP withdrawal does not give you the room back. The money comes out taxable and the room is gone for good, with narrow exceptions for the Home Buyers' Plan and the Lifelong Learning Plan, which are really loans you repay into the RRSP on a schedule.

TFSA vs RRSP carry-forward, side by side

If you only remember one table from this page, make it this one.

| Question | TFSA | RRSP |

|---|---|---|

| Does unused room carry forward? | Yes, indefinitely | Yes, until age 71 |

| Does it depend on income? | No | Yes (18% of earned income) |

| Backdated room for someone eligible since 2009 | $109,000 in 2026 | Depends entirely on past income |

| Do withdrawals restore room? | Yes, next January 1 | No (withdrawals are taxable and gone) |

| Over-contribution buffer | None | About $2,000 lifetime |

| Contributions reduce taxable income? | No | Yes (it's a deduction) |

That last row is the reason the two accounts exist side by side. A TFSA gives you tax-free growth and withdrawals with no deduction. An RRSP gives you a deduction now and taxes the money when you pull it out later. Neither is "better" in the abstract. It depends on your tax rate today versus in retirement, which is a personal question this page can't answer for you.

If you want to put rough numbers on that retirement question, two free tools from our sister site The Desk Brief help: the FIRE number calculator estimates the portfolio size you'd need before work becomes optional, and the compound interest calculator shows what today's unused room could grow into by the time you need it.

One more account confuses people on carry-forward, so it's worth a quick aside: the First Home Savings Account. If you're saving for a first home, the FHSA gives you $8,000 of room a year up to a $40,000 lifetime maximum. But its carry-forward is stingy next to the other two. You can only carry forward a single year's unused room, up to $8,000, and only once you've actually opened the account. Plenty of people assume it stacks like a TFSA. It doesn't, so opening one early just to start the clock is often the move.

How to find your real number

Don't guess, and don't trust a blog's running total over your own records. Your actual room is personal, and two official sources hold it:

- CRA My Account. Log in and you'll see both your TFSA contribution room and your RRSP deduction limit. This is the most current source the government gives you.

- Your Notice of Assessment. Your RRSP deduction limit for the year is printed right on your latest NOA, after you file.

Here's the honest caveat, and it matters. The CRA's TFSA figure is only as current as what financial institutions have reported, which usually happens once a year. So if you contributed or withdrew recently, the number you see can be out of date by months. I've seen people trust a stale CRA figure, top up to it, and accidentally over-contribute. Keep your own simple tally of every contribution and withdrawal with dates. It takes two minutes and it's the only number that's truly live. If you'd rather not log in, you can call the CRA's automated TIPS line or request a TFSA Room Statement, but both lean on that same once-a-year reporting, so they carry the same lag.

The mistakes that cost people money

Most contribution-room trouble comes down to a handful of avoidable errors:

- Re-depositing a TFSA withdrawal too early. You took $10,000 out in March to cover something, then put it back in November. Unless you had unused room to cover it, that re-deposit is an over-contribution, because withdrawn room doesn't return until the next calendar year. The penalty is 1% per month on the excess.

- Assuming you have the full $109,000. If you immigrated, turned 18 after 2009, or had non-resident years, your TFSA number is lower. Confirm it.

- Counting investment income as earned income for RRSP room. Dividends and capital gains don't build RRSP room. Employment and self-employment income do.

- Forgetting the pension adjustment. If you're in a workplace defined-benefit or defined-contribution pension, your RRSP room is reduced by a pension adjustment. Your NOA already accounts for it, which is another reason to trust the NOA over a back-of-napkin 18% calculation.

- Over-contributing on purpose to "get ahead." The TFSA has no buffer. There's no upside to going over, only a monthly penalty.

- Treating a TFSA like a day-trading account. If the CRA decides you're carrying on a business of trading inside your TFSA, it can tax the gains as business income. The tax-free wrapper isn't a license to run a brokerage.

- Contributing while you're a non-resident. You don't accrue TFSA room for non-resident years, and contributions made while non-resident carry their own 1% monthly tax. If you moved abroad and kept contributing, check this one carefully.

Once you know your room, what goes where?

Figuring out how much room you have is step one. Step two is deciding what to actually hold in each account, and that's a separate question with real tax consequences. The same stock can be a smart TFSA holding or a poor one depending on where its dividends come from and how they're taxed.

That's the whole reason this site exists. You can search any stock or ETF on the free Canadian stock screener and see the educational read for your TFSA, RRSP, and taxable account in plain language. A few starting points that pair well with this guide:

- Canadian stock account location: TFSA vs RRSP vs non-registered, the framework behind it all.

- US dividend stocks in a TFSA vs RRSP for Canadians, because that 15% withholding catch surprises a lot of people.

- Eligible vs non-eligible dividends and the dividend tax credit, which decides how a Canadian dividend is taxed outside registered accounts.

- REITs in a TFSA, RRSP, or taxable account, since REIT distributions aren't simple dividends.

- Or browse the account-location read for popular stocks directly.

Check a stock before you fill that room

You've got the room. Before you buy, see whether a stock fits better in your TFSA, RRSP, or taxable account.

Open the free stock screenerFrequently asked questions

Can I contribute to my TFSA for previous years?

There's no separate "previous year" TFSA contribution like there is for an RRSP at tax time. Unused room from every year you were eligible carries forward into one running total, so when you contribute today you're simply using up that backdated room.

Does unused RRSP contribution room expire?

No. It carries forward indefinitely, up to the year you turn 71. Just remember it's income-based, so you only build new room in years you had earned income.

How much TFSA room do I have if I never contributed?

If you were at least 18 and a resident every year since 2009, your 2026 cumulative room is $109,000. If you turned 18 later, add up the annual limits from that year on.

How do I find my exact contribution room?

Check CRA My Account or your latest Notice of Assessment, and keep your own tally of recent contributions and withdrawals since the CRA's number can lag.

Sources

Everything above is drawn from the CRA's own pages. Verify your situation against these:

- CRA: Calculate your TFSA contribution room

- CRA: Before you contribute to a TFSA (rules and over-contributions)

- CRA: MP, DB, RRSP, DPSP, ALDA, TFSA limits and the YMPE (official annual limits table)

- CRA: How contributions affect your RRSP deduction limit

- CRA: Tax-Free Savings Account overview

- CRA: RRSPs and related plans